A new survey reveals that most Veterans living with a VA disability rating are likely losing thousands of dollars by not maximizing the benefits they’ve earned. The most glaring evidence in the survey revealed that nearly three in four disabled Veterans are not aware of the thousands they could save on a VA loan funding fee exemption.

Other findings in the study highlight a widespread lack of awareness about disability-related programs and processes, which can cost Veterans and their families thousands of dollars in lost compensation, education benefits, or job training.

Key Points

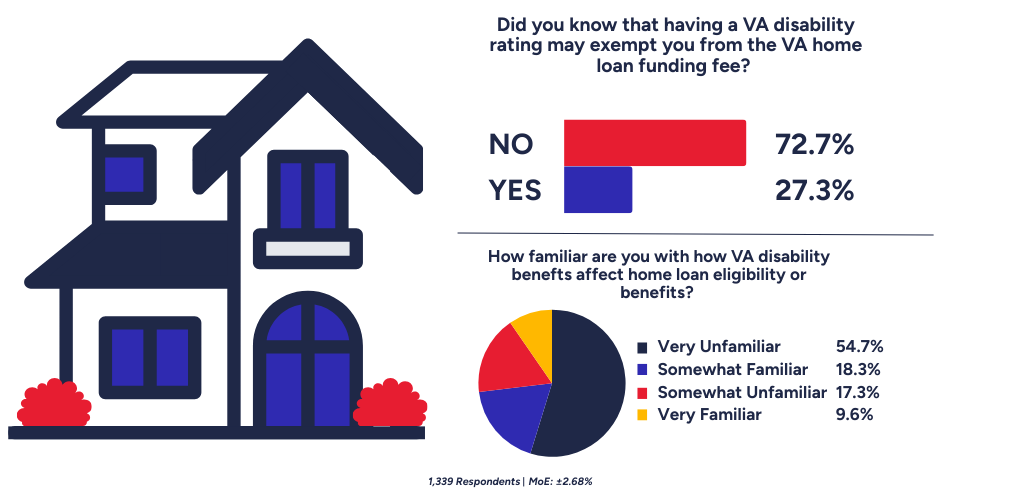

- 72% of Veterans didn’t know their VA disability rating could exempt them from the VA home loan funding fee, which could save thousands of dollars.

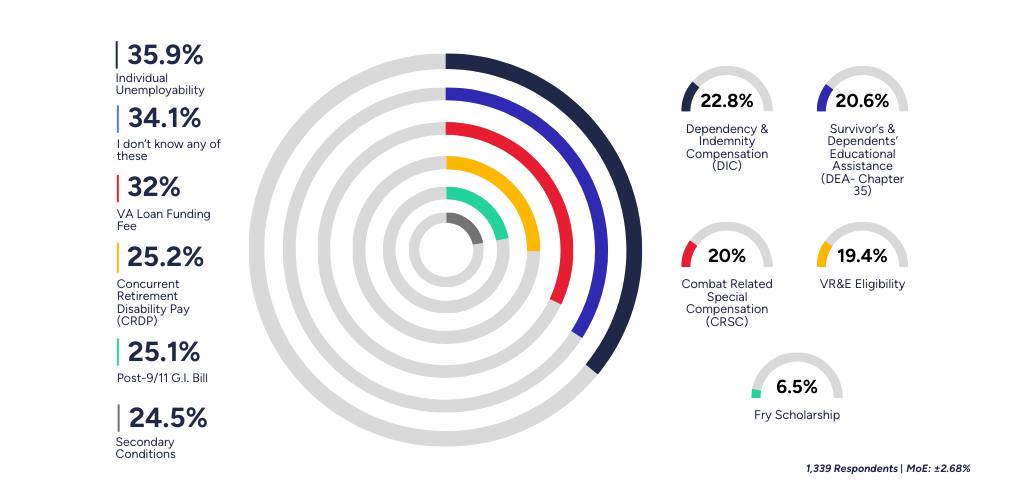

- Fewer than 3 in 10 Veterans knew about any of the 10 major VA programs offering extra monthly payments, education, or job training worth tens of thousands over a lifetime.

- Nearly 60% were unfamiliar with the appeals process, risking missed opportunities to increase their compensation.

Missed Financial Benefits

The Veteran Voices Summer Feedback Giveaway aimed to gauge respondents’ knowledge of the VA’s disability program and other programs available to Veterans with disabilities. The home loan finding was only part of the story. The survey revealed that awareness of other major VA disability-linked programs was equally low:

- Individual Unemployability: 35.9%

- VA Loan Funding Fee Waiver: 32%

- Concurrent Retirement Disability Pay (CRDP): 25.2%

- Post-9/11 G.I. Bill (linked to disability): 25.1%

- Secondary Conditions claims: 24.5%

- Dependency and Indemnity Compensation: 22.8%

- Survivors and Dependents’ Educational Assistance: 20.6

- Combat Related Special Compensation (CRSC): 20%

- VR&E Eligibility: 19.4%

- Fry Scholarship: 6.5%

The low awareness of these programs suggests that many Veterans may be missing out on valuable financial assistance for housing, education, job retraining, or support for their dependents.

Real World Example: Education Benefits

Suppose you’re a Veteran with a disability rating but want to get your education for a civilian career post-service. In that case, numerous VA benefits can help you pay for college, additional technical training or job training, job placement services, monthly housing costs, and other perks that can save you thousands and make it easier to afford owning your own home. All of that in addition to your monthly tax-free VA disability compensation. So let’s break it down.

Scenario: You live in Louisiana, and received a VA disability of 30% after separating from active duty. You want to attend school full-time and earn your bachelor’s degree at LSU, using that education to launch your civilian career. You also hope to rent during your time in college and buy a home once you’re finished with your education.

Possible Veterans Benefits (College)

| Benefit | Amount | Program |

|---|---|---|

| VA Disability Compensation | $537.42 / Monthly | VA Disability Benefits |

| College Tuition and Fees | $12,472 (In-state tuition level for LSU) | Post-9/11 G.I. Bill Program |

| Books | $1,000 | Post-9/11 G.I. Bill Program |

| Rent / Monthly Housing Allowance (MHA) | $1,839 / Monthly (during the 9-month school year) | Post-9/11 G.I. Bill Program |

Scenario Expenditures (College)

| Expenditures | Amount |

|---|---|

| Campus Meal Plan* | $5,400 (Annually) |

| Books | $1,084 (Annually) |

| Rent (Off-Campus) | $1,100 per month (12 months) |

*-optional

So if you’re going to a four-year university and living off-campus, you’ll have $12,472 per year in tuition and fees, $13,200 in rent, $1,084 in books, and $5,400 in food costs if you buy a campus meal plan, if you want that option. That brings your total to $32,156 in costs, excluding any social life expenditures, groceries, gasoline, parking, and utilities (including electricity, internet, and gas).

However, your VA benefits would cover the $12,742 in tuition. It covers all but $84 per year for books. It provides you with MHA for 9 months, which totals $16,551 for the year, and pays you $537.42 per month for your VA disability.

This means that over those 12 months, you receive $36,472 in benefits, leaving you with a little over $4,000 in extra funds. That also doesn’t include any money you may make from a part-time job or job/internships during the summer break.

If you take those costs over 4 years, add roughly a 2% COLA increase to your VA disability each year, a 1.4% increase in MHA each year, a 3% increase in tuition, and a 2% increase in rent, you’d get a final breakdown like this:

Possible VA Benefits (4 Years of College)

| Year | Paid Tuition & Fees (Annually)*3% Annual increase | MHA (over 9 months)*1.4% Annual Increase | Book Stipend (Annually) | VA Disability payments (Annually)*2.5% Annual Increase | Total Benefits Paid (Annually) |

|---|---|---|---|---|---|

| Year 1 | $12,472.00 | $16,551.00 | $1,000 | $6,449.04 | $36,472.04 |

| Year 2 | $12,846.16 | $16,782.71 | $1,000 | $6,610.27 | $37,239.14 |

| Year 3 | $13,231.54 | $17,017.67 | $1,000 | $6,775.53 | $38,024.74 |

| Year 4 | $13,628.49 | $17,255.92 | $1,000 | $6,944.92 | $38,829.33 |

| Total | $52,178.19 | $67,607.30 | $4,000 | $27,779.76 | $150,565.25 |

**-Year 1 totals align with 2025 rates

Expenditures (4 Years of College)

| Year | Paid Tuition & Fees (Annually)*3% Annual increase | Rent (Off-Campus Annually)*2% Annual Increase | Books (Annually)*3% Annual Increase | Optional On-Campus Meal Plan (Annual)*3% Annual Increase | Total Costs Paid (Annually) |

|---|---|---|---|---|---|

| Year 1 | $12,472.00 | $13,200 | $1,084 | $5,400 | $32,156.00 |

| Year 2 | $12,846.16 | $13,464 | $1,116.52 | $5,562 | $32,988.52 |

| Year 3 | $13,231.54 | $13,733.28 | $1,150.02 | $5,728.86 | $33,843.70 |

| Year 4 | $13,628.49 | $14,007.94 | $1,184.52 | $5,900.73 | $34,721.68 |

| Total | $52,178.19 | $54,405.23 | $4,535.06 | $22,591.59 | $133,709.90 |

**-Year 1 totals align with 2025 rates

The comparison over four years shows that the benefit programs would provide over $150,000 in value. However, this example does not account for the costs associated with daily life, such as utility bills, parking, gasoline, and groceries. However, it does show a leftover amount each year that could easily cover most annual utility costs. That leftover money increases if you choose to opt out of the meal plans and instead buy more groceries or eat off campus.

That amount only covers college. Other examples include job training and job placement programs, which disabled Veterans can access through the VA’s Veteran Readiness and Employment (VR&E) program. This offers hours of access to programs that help lead to job placement for disabled Veterans entering the civilian workforce.

Real World Example: VA Loan Program

Other programs available involve the VA loan program, which offers Veterans with a disability rating an exemption on VA loan funding fees. That can amount to thousands of dollars off your home loan amount, thus lowering your monthly payment and the amount you pay over the life of the loan.

Scenario: Following the previous example, you went to LSU on the G.I. Bill. Now, let’s imagine you’ve gotten married and want to buy a house in the Baton Rouge area. First, you’re VA disability payment increases due to you adding a dependent. Next, you find a house that you and your spouse want that costs roughly $232,000. With the benefit of a VA loan, you’re not responsible for paying the VA loan funding fee. The VA loan funding fee is a payment each VA loan borrower must pay as part of the loan. Oftentimes, it is rolled into the VA loan amount.

VA Loan Funding Fee Exemption

| Item | Cost to Veteran with no Disability Rating | Cost to Veteran with a Disability Rating |

|---|---|---|

| VA home loan | $232,000* | $232,000* |

| VA Loan Funding Fee | $4,988 (first-time VA loan user) | $0 (Exempt with 10% or higher VA disability rating) |

| Estimated Monthly Payment | $1,739 per month** | $1,709 per month** |

| Life of the Loan | $626,040*** | $615,356.32*** |

*- denotes 0% down payment

**-denotes 6.125% interest rate, 1.2% property taxes, and a .35% insurance rate

***-denotes an amortization estimate of 30 years of monthly payments with no refinances

In this hypothetical example, you can see that the first benefit is that if you’re living with a VA disability rating, you’re immediately saving nearly $5,000 in mandatory costs for a VA loan, which would translate into $30 less per month in mortgage payments. Note: The funding fee percentage jumps after your first VA loan, so in this scenario, your funding fee payment would have been roughly $7,600.

The last row in the table highlights a factor that many may not consider when getting a loan. It’s the impact that even $30 additional dollars a month can have on a 30-year mortgage. After 30 years, a standard amortization schedule shows that over those 30 years, you’ll have paid more than $10,000 less if you have a VA disability rating!

Disability Ratings, Appeals, and Secondary Conditions

The survey showed that lack of awareness isn’t limited to programs but also extends to the processes that determine VA disability ratings. This awareness is important because the ratings affect monthly compensation.

Appeals Process

Nearly 60% of Veterans were unfamiliar with the appeals process. Among those who appealed, half won an increase, while nearly one-third were denied. Many Veterans who never appealed may have missed out on higher pay simply because they didn’t understand the process.

Combined Ratings

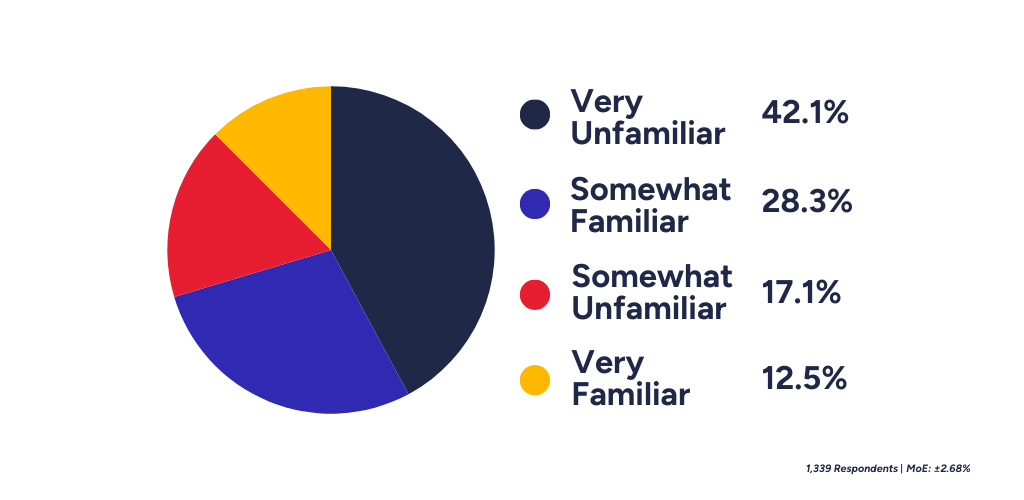

Combined disability ratings are based on a specific formula that the VA uses to determine VA ratings if someone files a claim with multiple injuries or conditions. However, almost half of the respondents were “very unfamiliar” with how combined ratings work.

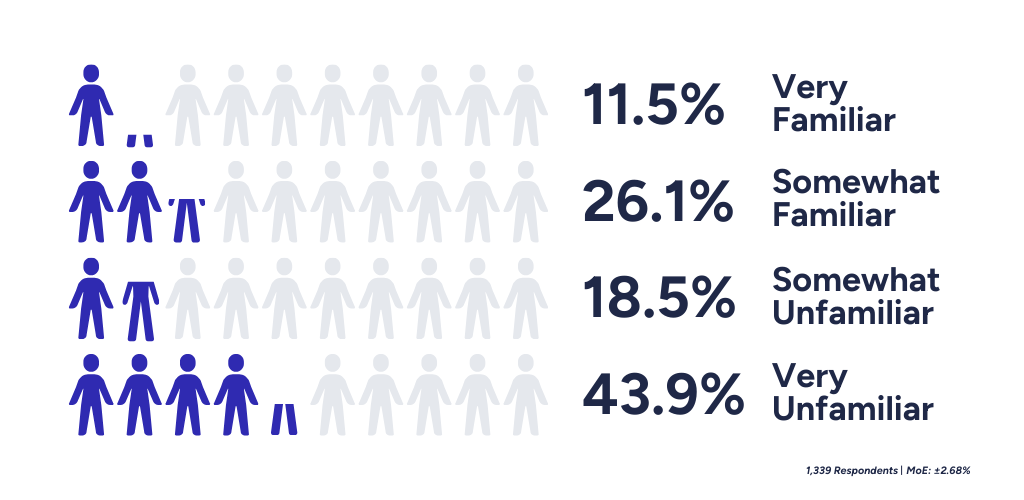

Combined ratings often involve secondary conditions because they’re in addition to the main injury or condition in the original disability claim. If approved during the claims process, secondary conditions could lead to an increase in VA disability rating and thus increased monthly VA disability compensation. This could mean several hundred, if not thousands, of dollars each month that aren’t being fully utilized. However, more than half of the respondents claimed they were unfamiliar with the process of filing for “secondary” conditions.

Dependents and Compensation

Dependent status is another key area where some Veterans lose out on financial benefits. The survey found that 44% of Veterans didn’t know that life changes like marriage, divorce, or having a child affect disability pay. Adding or removing dependents affects monthly compensation. Adding dependents increases your monthly VA disability payment. However, not removing them if a child ages out, or not removing someone if you get divorced, could also cost you money because of the cost of paying back your overpayment if the VA finds out you’re no longer married, and receiving a boost due to dependent status. However, 77% knew they could receive extra compensation for dependents.

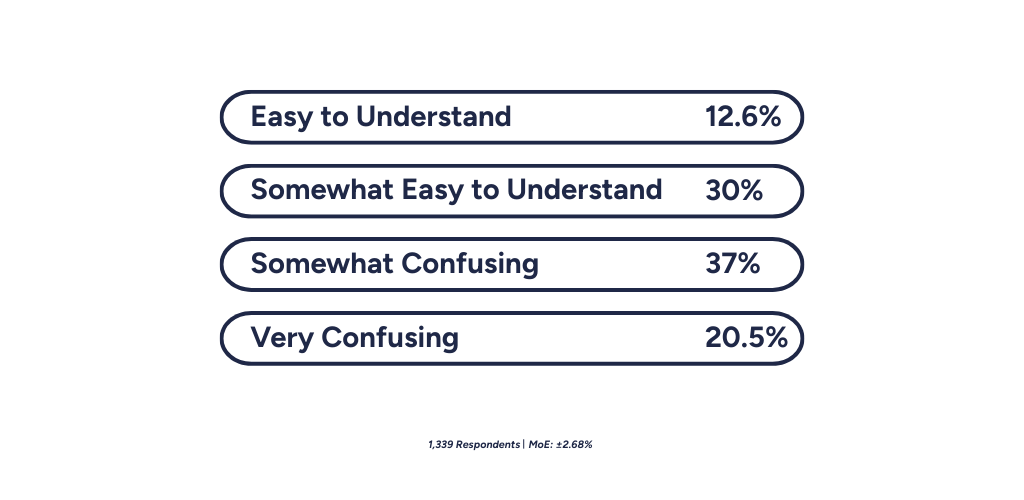

Filing Alone and Paperwork Confusion

VA paperwork was another roadblock. More than half of respondents reported that the forms were confusing, with only 12% finding them easy to understand. That knowledge, coupled with the filing process, can also lead to lost opportunities. The survey found that 44% filed claims on their own, while another 25% were unaware that free help from a Veteran Service Organization (VSO) was available. Choosing to file without help, or not knowing help exists, leaves Veterans more vulnerable to mistakes, delays, and lost benefits.

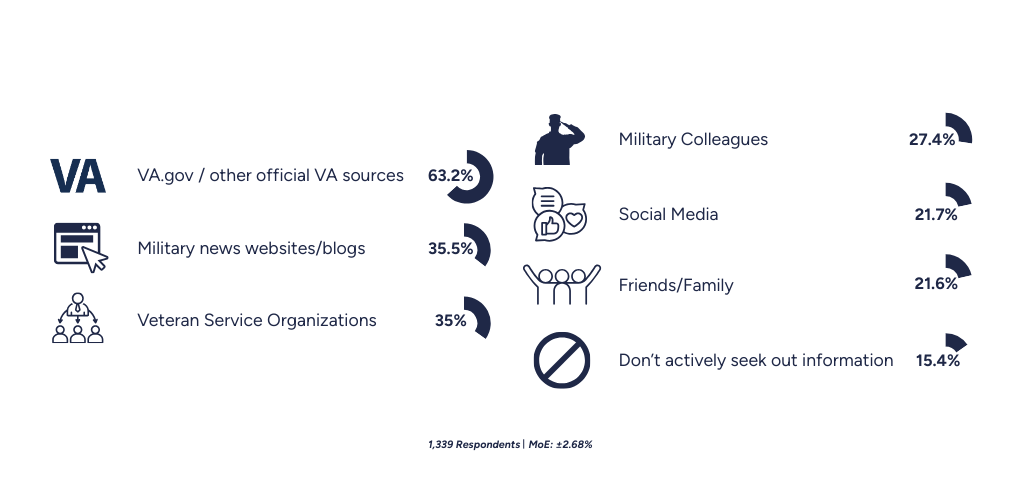

Where Veterans Get Information

Most rely on VA.gov (63%) for benefits information, followed by military news sites (35%) and VSOs (35%). But despite these sources, many respondents said they wished they had known more before filing, especially about benefits that could have saved or earned them thousands.

Conclusion

The 2025 Veteran Voices survey highlights a serious concern: Veterans are often unaware of the benefits and processes that could put more money in their pockets.

From appeals and secondary conditions to dependents and home loan fee exemptions, lack of awareness translates directly into lost financial security. Veterans are filing claims alone, struggling with paperwork, and leaving education, housing, and monthly payments on the table.

Methodology Summary

The survey, hosted on Typeform, was conducted from July 1 to July 29, 2025. Invitations were sent to the 96,000+ subscribers of the Veteran.com email list, and the survey was also posted publicly. In total, 1,945 people started the survey, and 1,339 completed it (completion rate: 68.8%).

The survey included 31 questions with logic branching, meaning not all participants saw the same questions. Only fully completed surveys were analyzed. No results were weighted. The margin of error at a 95% confidence level was ±2.7% for large groups, with higher margins for smaller groups.

-

Jon Rehagan is a 2-time Emmy Award-winning journalist who covers financial topics and military news for the veteran community. With 16 years in broadcast media (including roles in radio and television) Jon has spent his career writing, shooting, editing, and producing everything from long-form investigative specials to daily news broadcasts and digital content. His work has been recognized by the Kansas Association of Broadcasters, and he brings that same commitment to accurate, accessible reporting to helping service members, veterans, and military families navigate complex benefits and financial decisions.