March 2026 Update: Lawmakers modified the original bill that would have stripped the VA disability VA loan funding fee exemption for some veterans. The House Committee on Veterans Affairs amended the policy to keep the VA disability VA loan funding fee exemption in place for all veterans with a disability rating, regardless of their rating percentage.

However, the amendment changed the VA loan funding fee amounts slightly, which may still affect veterans trying to use a VA loan to buy a home.

The main point: The legislation now makes it so If you plan to use a VA loan, you would continue paying current funding fees for about two additional years, until September 30, 2036. Originally, the VA loan funding fees were set to decrease in 2034. This change keeps purchase loans, especially those with little or no down payment, at today’s rates for longer.

The updated policy would raise refinancing and loan assumption costs. The changes would be the following:

- VA streamline refinance: VA loan funding fee would increase from 0.5% to 1.4%

- Assuming a VA loan: VA loan funding fee would increase from 0.5% to 1.0%

So, for example, for a VA streamline refinance on a $ 300,000 loan, the cost increases from $1,500 to $4,200 ($2,700). Using the same loan amount, if you assume an existing VA loan, the fee would rise from $1,500 to $3,000.

If you qualify for a funding fee exemption, these changes may not affect you, but many borrowers would face higher upfront costs when buying, refinancing, or assuming a VA loan. The policy is a proposal aimed at generating more revenue that would be used to fund benefit increases for survivors and catastrophically disabled veterans.

Original Proposal Regarding VA Loan Funding Fees

The changes to the program are part of H.R. 6047, known as the Sharri Briley and Eric Edmundson Veterans Benefits Expansion Act of 2025. If passed and signed into law, it would modify the VA home loan funding fee requirements starting August 1, 2026.

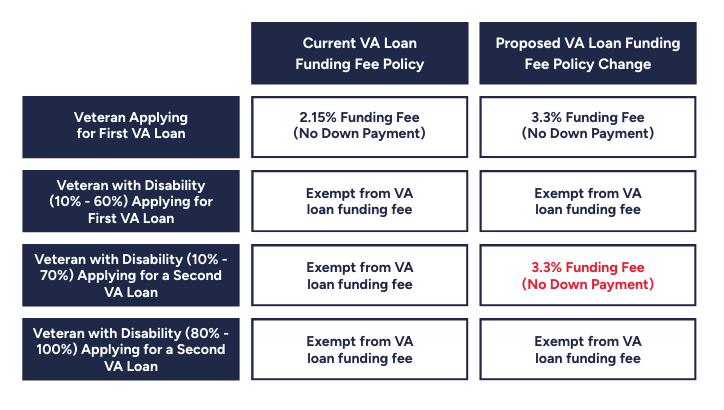

The proposed legislation would require veterans with disability ratings of 70% or less to pay the standard 3.3% funding fee when taking out subsequent VA loans. First-time VA loan users with disability ratings of 70% or less would still remain exempt from the fee. The exemption would continue to apply in full to veterans with disability ratings of 70% or higher.

Note: Veterans using a second, or subsequent, VA loan do not necessarily mean they’re getting access to a VA loan to buy additional properties. The VA loan program is designed to help veterans purchase homes where they will reside, not vacation homes or rental properties.

The Current VA Funding Fee Policy

Under current law, if you live with any service-connected disability rating, you are exempt from paying the VA funding fee. It currently helps veterans living with disabilities save thousands of dollars when buying a home.

Financial Impact for Affected Veterans

For veterans with disability ratings of 70% or less who plan to use their VA loan benefit more than once, this change could represent a significant financial impact.

Example: You have a 60% disability rating and want to buy a $500,000 home using your VA loan for the second time. Right now, you pay zero in funding fees because you receive VA disability compensation. Under the proposed changes, you’d pay a 3.3% funding fee, totaling $16,500. You can add this fee to your loan instead of paying it up front, but you’ll pay interest on it for the next 30 years.

Note: If the bill passes, completing your transaction before August 2026 could save you thousands of dollars in funding fees.

Understanding the VA Funding Fee

The VA funding fee is a one-time payment that helps cover the cost of the VA loan program for taxpayers. If you don’t have a disability rating, you’ll pay between 2.15% and 3.3% of your loan amount, depending on whether it’s your first VA loan and how much you put down. Right now, if you receive VA disability compensation, you don’t pay this fee at all, no matter what your rating percentage is.

Why Congress Is Considering This Change

The funding fee modification isn’t happening in isolation. It’s being used as a way to offset the costs of two substantial benefit increases for VA disability recipients.

First, the legislation would increase Special Monthly Compensation for catastrophically disabled veterans who require aid and attendance. If you or your veteran qualifies for this benefit, you’d receive an additional $833.33 per month (that’s $10,000 more per year).

“This critical improvement will positively impact the lives of our most vulnerable veterans and provide much-needed financial support for their families, who must shoulder the immense responsibility of caregiving,” according to testimony from the Tragedy Assistance Program for Survivors (TAPS).

Second, the bill would provide surviving spouses with their first base rate increase to Dependency and Indemnity Compensation (DIC) since 1993, in addition to the annual cost-of-living adjustments they already receive. If you receive DIC, your benefit would increase by an additional 1% per year for five years, raising it from 43% to 48% of the benefit received by a 100% disabled veteran.

The Budget Rules Challenge

The reason Congress is considering the VA funding fee as a revenue source stems from House budget rules. At the beginning of the 119th Congress, the House adopted rules requiring any new spending to be offset by spending cuts or revenue-generating programs within the committee’s jurisdiction.

For the House Veterans’ Affairs Committee, the VA home loan funding fee is one of the only available mechanisms to fund new initiatives or offset benefit expansions. This puts the committee in a difficult position: how can benefits be expanded for one group of veterans without negatively impacting another?

Veteran Organizations Have Concerns

Major veteran service organizations support the benefit increases but have expressed serious reservations about the funding mechanism.

The American Legion, in testimony submitted to the House Veterans’ Affairs Committee, stated its opposition clearly: “The American Legion remains deeply concerned with the funding fee provision proposal and strongly urges the Committee to explore alternatives to provide adequate funding.”

The organization pointed to its longstanding position opposing the existence of the VA funding fee entirely. “Resolution No. 314: Support Elimination of the VA Home Loan Funding Fee directly states, ‘The American Legion supports the elimination of the Department of Veterans Affairs (VA) Home Loan funding fee,” their testimony noted.

The American Legion also raised concerns about the broader precedent: “We are concerned with the potential precedent this change would set for future funding for benefits being derived from other groups of veterans.”

The Veterans of Foreign Wars (VFW) raised additional concerns in their testimony, warning that “imposing fees on those below that threshold would create a two-tiered system of worthiness based on disability percentage. Yet all disabled veterans earned their benefits.”

An Alternative Funding Approach

The American Legion has proposed an alternative funding mechanism: expanding VA loan eligibility to allow veterans to transfer their home loan benefit to certain dependents. That plan is fueled by the idea that this change would increase the number of people using VA loans and generate additional funding fee revenue without requiring disabled veterans to pay fees they’re currently exempt from.

“Expanding the VA Home Loan benefit to include transferability promotes financial stability and supports the well-being of veterans and their families, especially in the case of the veteran’s death,” The American Legion testified.

This approach would generate revenue from a new user base rather than removing an existing benefit from current users. However, it’s unclear whether this alternative would generate sufficient funding to offset the proposed benefit increases.

What Happens Next

Now lawmakers needs to review the amendments, and discuss it to see if it can pass out of committee and go up for a House vote. If the bill were to be passed into law, the changes would take effect on August 1, 2026, and would remain in place through September 30, 2036.

This amended language now means if you’re considering a streamline refinance of your VA loan, or if you’re considering a home purchase where you assume a VA loan, you may have to pay more.

We’ll continue to montior this legislation as it works it way through Congress.

Your military benefits make homeownership more affordable—$0 down, no PMI, and lower average rates whether you’re buying or refinancing. See if you're eligible today.

-

Jon Rehagan is a 2-time Emmy Award-winning journalist who covers financial topics and military news for the veteran community. With 16 years in broadcast media (including roles in radio and television) Jon has spent his career writing, shooting, editing, and producing everything from long-form investigative specials to daily news broadcasts and digital content. His work has been recognized by the Kansas Association of Broadcasters, and he brings that same commitment to accurate, accessible reporting to helping service members, veterans, and military families navigate complex benefits and financial decisions.